A No-Landing Economy, the ESG Train to Nowhere, and Jamal Murray Crushing LA

April 23, 2024

The "No-Landing" Scenario

The Fed is in a tricky spot. People hate inflation but they also hate high interest rates. What’s a central banker to do?

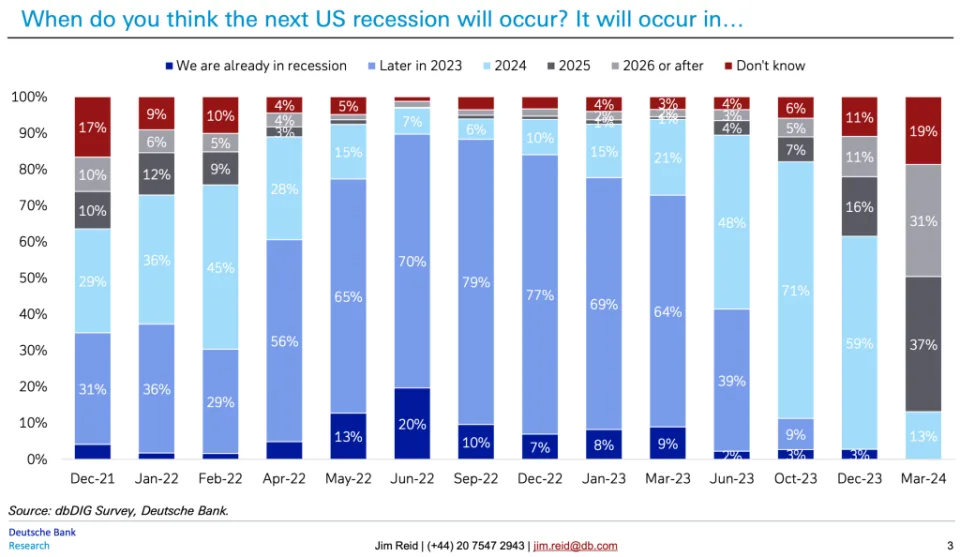

Some speculate that interest rate cuts will not transpire until November, and 45% of investors feel the economy is headed neither to a soft nor hard landing (Deutsche Banks’s March Global Markets Survey).

So what’s the third alternative? The plane simply keeps flying, fuel be damned, to a “no-landing” scenario where inflation fails to maintain a downward trajectory (or even re-accelerate) amidst robust economic expansion and the Fed holding interest rates steady for the time being.

Uncertainty Abounds

When asked to predict when the next recession will occur, an increasing percentage of investors responded that they “do not know.” Uncertainty is not good for markets.

The Road to a Soft-Landing

Between a hard landing and a ghost plane to nowhere, a soft landing is the preferred destination. In fact, Alan Greenspan orchestrated a classic soft landing in the mid-1990s.

In February 1994, the US economy registered low unemployment, with CPI inflation at 2.8% and the federal funds rate at roughly 3%. The country was approaching its third year of recovery after the 1990-91 recession, and with the economy heating up and unemployment continuing to decline, Greenspan was concerned about the risk of inflation.

As a result, the Fed raised rates seven times that year, doubling the federal funds rate to 6%. In 1995, the funds rate was cut three times when the economy began to soften more than required to keep inflation from rising.

The remainder of the 90s made Greenspan a central banking legend - unemployment trending downwards, low and steady inflation, and average real GDP growth above 3% per year.

Recessionary Psychology

Compared to February 2020, we’re spending 20% more on milk, 30% more on bread, and 50% more on eggs. Rents are up over 20%, and electricity has ballooned by 30%. Not surprisingly, people are turning to easy credit to get by.

The average credit card APR is a record high of 20.75%. Paying off $5,000 in debt at this rate would take 279 months and $8,124 in interest.

The flip side, however, is that U.S. incomes, on average, have risen to equal or greater levels than the increased costs for services and goods. Inflation is also down from previous highs, but psychologically, we always pay more attention to how much we’re spending as opposed to how much more we’re bringing in.

For many Americans under 40, inflation at these levels is new. The last time inflation was close to double digits was the early 1980s, and nimble monetary policy of interest rate cuts and increases has helped the Fed hit its target of 2% for the most part over the past 30 years.

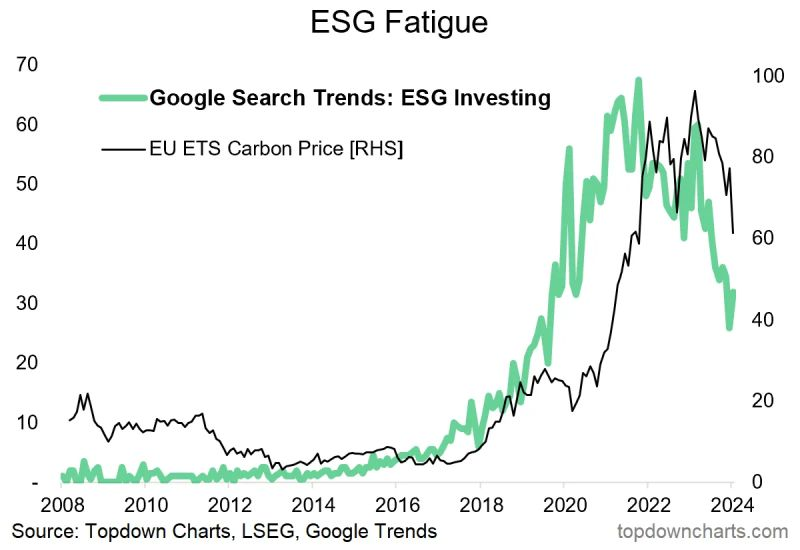

The Slowing ESG Train

In hindsight, ESG was too large of a catch-all. Environmental, social, and corporate governance - that’s a heck of a basket of goods!

The percentage of newly created funds in Europe and the US with ESG as part of their name is now 3.3% (down from a peak of 8.3%).

Likewise, Google searches have faded.

One reason might be lagging growth in EV sales and a host of shelved clean energy projects. The S&P Global Clean Energy index has lost 31% since early 2023, compared with 27% positive returns for global stocks.

Companies are shying away from even mentioning ESG during earnings calls.

There’s much to unpack, but I always found the manner in which ESG ratings were provided was suspect in itself.

This paper from the Leibniz Institute SAFE found different ratings agencies providing quixotically different scores to the same companies.

Keep an eye on BlackRock. They’ve dropped ESG and are now emphasizing “transition themes.”

Lastly, despite growing up in LA, the family was always a college basketball family - not big into the NBA. But with the Lakers as your home squad, it's hard not to root for the Lake Show, and when shots like this happen, you sense the end is near ...